Introduction

The credit score is the first factor to assess if one qualifies for a loan. A credit score is a three-digit numerical summary of the entire credit history created by CIBIL (Credit Information Bureau, India Limited). It is based on the data banks and other financial institutions provide to CIBIL regularly. A person’s credit score typically falls between 300 and 900. Both credit score and credit history will be checked by the bank as soon as one applies for a loan and submits the completed loan application.

Banks will outright refuse loan applications from borrowers with poor credit histories and low credit scores. But if the credit rating is high, the bank will approve the loan application immediately and move on to the next step.

The CIBIL / credit score is the primary determining factor in whether or not the loan application will be approved. Therefore it is crucial to understand the factors affecting CIBIL score and take the necessary actions to raise it if it is below expectations.

5 Factors That Affect CIBIL Score

The CIBIL score is impacted by various things. However, the five main factors that explain how the CIBIL score is affected are:

1. Financial History

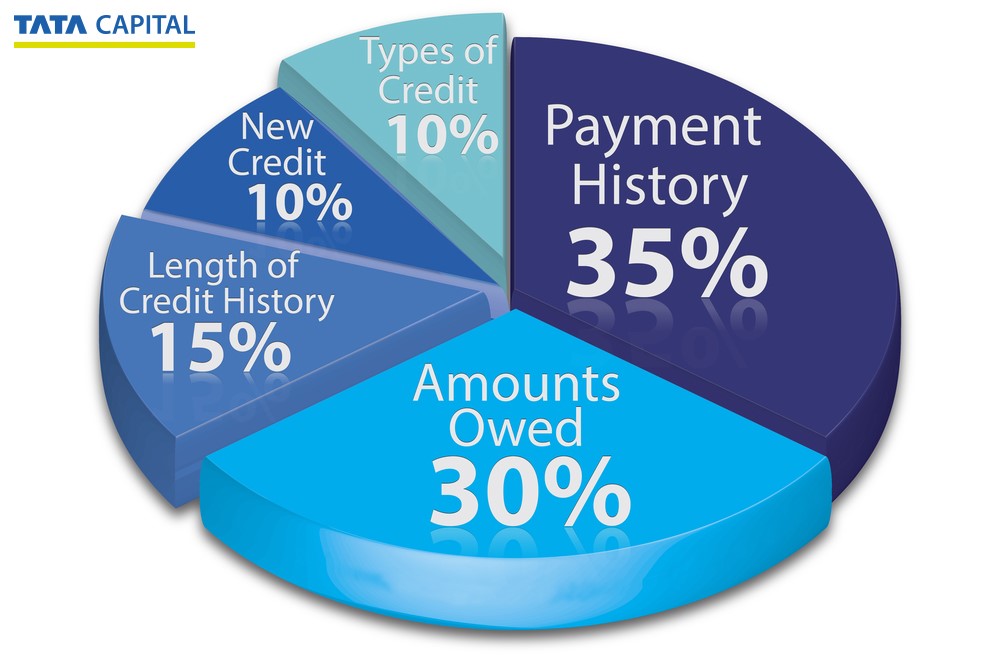

One of the most crucial factors affecting CIBIL score is one’s payment history. Flawless payment history shows that they are a trustworthy borrower. As the lender is confident in their ability to pay back the loan, they may provide one with the best possible terms and interest rates. Therefore, be sure to make all payments on time.

Keep track of monthly bills to ensure they are all on schedule. Even an honest oversight that results in a payment default lowers the CIBIL score. Use tools like auto-debit, standing orders, or NEFT mandates to guarantee that monthly EMI payments are completed on time. The payment history is the biggest factor that affects the CIBIL score.

2. Credit Mix

One of the most popular CIBIL score affecting factors used to determine credit ratings is credit mix or the variety of credit accounts. Several credit accounts, such as a house loan, personal loan, and credit card, demonstrates to lenders the ability to manage various forms of debt concurrently.

Additionally, it aids in improving the comprehension of their financial position and willingness to make debt payments. Although having a less varied credit portfolio wouldn’t always result in worse scores, the more different forms of credit one have, the better. An individual’s credit mix, which makes up 10% of their score, can contribute to getting a good one.

3. Paying the percentage of outstanding credit

Paying merely the bare minimum due is one of the factors affecting the CIBIL score poorly. A tiny part of each month’s total billed amount is the minimum amount that must be paid. If the minimum payment is made, interest continues to accrue on the balance due. If interest starts accruing to the unpaid debts, it becomes unlikely to manage to pay off the entire amount since it grows to be rather large. This practice may cause one to slide into a debt trap quickly, and it will be tough to escape this vicious circle of debt once someone enters it. It shows carelessness with debt and making bad repayment decisions. Therefore, if an individual doesn’t want to get the CIBIL score affected negatively, it’s crucial to make the payments in time and in full. If they cannot pay the whole amount, they must pay the most they can, which should always be more than the minimum amount due.

4. Excessive Credit Use

One of the factors affecting the CIBIL score is excessive credit use. The credit usage ratio, expressed as a percentage, reveals how much of the available credit has already been utilized. Whatever the credit card limit of an individual is, one should only use 30% of this maximum limit. If one wants a higher credit score, then keep the credit ratio low.

5. Multiple Applications For Credit Cards

Multiple applications for credit cards are one factor that affects CIBIL score. Before processing a request for a credit card, any financial institution will compile a credit report to examine one’s credit score. A hard inquiry is a term for this kind of investigation. Each time this kind of query is made, the CIBIL score gets affected negatively.

Therefore, if one has applied for credit cards from many institutions, many hard inquiries will be made about them, severely lowering their credit score. That is why one should refrain from sending out many requests simultaneously. Don’t rush to apply for a credit card with a different bank if an application has been refused. Spend some time initially raising the credit score before submitting a credit card application.

Wrapping Up

The CIBIL score is an essential criterion to determine whether a person is sufficiently creditworthy to be awarded any credit. A strong CIBIL score gives more possibilities for decent credit cards with more sophisticated features and advantages. On the contrary, a low CIBIL score would make it harder for one to get a sound credit card. Having a decent credit score, often above 750, is crucial to take advantage of better lending options.

In this blog, we have discussed some important aspects of the CIBIL score such as how CIBIL score is affected by various factors. It is crucial to consider these aspects if one wants to have a decent CIBIL score.

5 mins read

5 mins read