Not only did the pandemic teach us a few hard-hitting life lessons, but it did teach us some valuable investment lessons as well. Little did we think that we had to learn it the hard way! Here are the top 5 investment lessons that changed my perspective about investing and financial planning.

1. Hedge your health risk properly

As we continue to see relatives, friends and family running pillar to post to settle their hospital bills, the magnitude of importance of health insurance was pretty evident. Finding a hospital bed was not the only problem that India had to face during the pandemic. It is disheartening to learn that a major part of the Indian population do not have any form of health insurance.

While this plagued the poor and the lower-middle class, even the rest of the population who had a cover extended by the employer fell short of the means to cover the humungous hospital bills. Many of the health insurance coverage needs to be rationalised to ensure that it aligns with the existing hospitalisation costs.

If you are covered by your employer, then you need to evaluate whether the cover is sufficient. Ideally, you will have to avail a separate medical cover externally from a competent insurer to cover the gap for yourself and your family.

2. Emergency corpus to keep the show running

The pandemic also saw a lot of job losses and downsizing, many individuals who had not prepared for such a situation were in dire need of funds to carry on with their household expenses. Many of them used their credit card for such emergencies, which is by far the most cardinal mistake and is just a preamble to fall into a debt trap, that could engulf your mental peace.

As a first step towards financial planning, you must always hold at least 6 months of household and emergency requirements in highly liquid form, preferably cash in your bank account. This should ensure that your house expenses and any of the other critical expenses such as children tuition fees, ongoing EMIs do not get affected in the unforeseen event of job loss or temporary loss of pay. Such emergency corpus will come in handy to manage the household before you find another job.

Additional Read – Money Lessons from the second COVID wave

3. Diversify your portfolio

Many people tend to put all their money in conventional investments, during the onset of the pandemic, it was feared that the markets would crash and burn in the backdrop of lockdown and lack of economic activity. Numerous investors stopped investing in equities and even pulled out their funds to save themselves from a probable steep fall. However, the ones who were in zen mode during such time had a field day, the markets reached unprecedented highs. The macroeconomic scenario remained grim and the interest earned on the conventional products were lower than expected. From the above instance, it is apparent that different instruments tend to perform well during different economic cycles. For a layman, it may be tough to ascertain the asset class which would provide good returns and move funds there frequently. The best one can do is to diversify the portfolio.

Many of the asset classes have an inverse correlation with the other asset classes, thereby ensuring that during a sharp downturn in any of the markets, the portfolio remains insulated due to the exposure in the other asset class. A classic example here would be the inverse correlation between equity and gold.

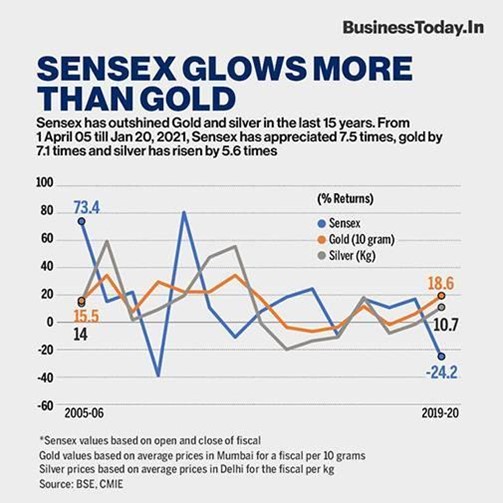

Source: https://www.businesstoday.in/markets/market-perspective/story/sensex-outshines-gold-in-journey-to-50000-mark-285020-2021-01-21

4. Budget your expenses

During the pandemic, the online sales of retailers grew by 2x – 9x times, which is indicative of people resorting to retail therapy to overcome the mental stress caused by lockdown, travel restrictions and other covid related challenges. These are easy financial traps that one can succumb to, we must remain responsible for our financial wellbeing despite challenging situations. We must always evaluate discretionary purchases on the scale of need vs. want.

Start with a budget that you will adhere to, this will ensure that you do not overspend, make impulsive buys. There are numerous mobile applications that will help you get started in this regard. As a thumb rule, always plan your discretionary spending after your investment commitments, EMIs, household expenses and building corpus for financial milestones.

Additional Read – Trailing V/S Rolling returns: Which one is a better indicator of fund performance?

5. Portfolio rebalancing at regular intervals

Portfolios have to be aligned as per changing personal needs and evolving market / economic scenarios. Hence, always practice consistent monitoring of your portfolio and seek the help of a professional to rebalance the portfolio, especially if you do not have adequate knowledge of the market dynamics/investment aspects.

Professionals at TATA Capital Wealth can guide you through the entire process of effective and efficient planning which will not only help you optimise your returns but will also see you through challenging times such as these.

5 mins read

5 mins read